So, What Are My Options?

Washington state offers different loan options and down payment assistance (DPA) programs for Washington residents looking to buy a home. Each program comes with certain requirements a buyer must meet to qualify, such as an income maximum limit or a minimum credit score. Those who qualify may pair a loan option with DPA.

There are two main loan options Washington state offers: Home Advantage and House Key Opportunity. Both programs offer the benefit of lower interest rate options, but the main key difference is that House Key Opportunity is open to First Time Buyers only, whereas Home Advantage is open to anyone who meets the stipulated requirements.

House Key Opportunity Loan

This loan program is only for first time buyers, or those buying in a target area (click here for WA state target areas). A first time buyer is defined as someone who has not owned or lived in a primary residence in the last 3 years. In addition to meeting either of these qualifiers, the buyer must use a Down Payment Assistance program or be purchasing new construction. They must also meet current income limits and not exceed certain loan amounts (those maximums can be found here).

Home Advantage

This loan program is for buyers whose household income does not exceed $180,000 statewide. If the buyer’s household income is 80% of a specific Area’s Median Income (AMI), they can qualify for additional interest rate options. This program can be used in addition to DPA, but does not have to be. Interest rates and 80% AMI limits can be found here.

Home Advantage may also work hand-in-hand with Washington’s new EnergySpark program, which gives buyers purchasing an energy-efficient home or making energy efficiency updates to an older home upon purchase 0.25% off of their interest rate. See the details here.

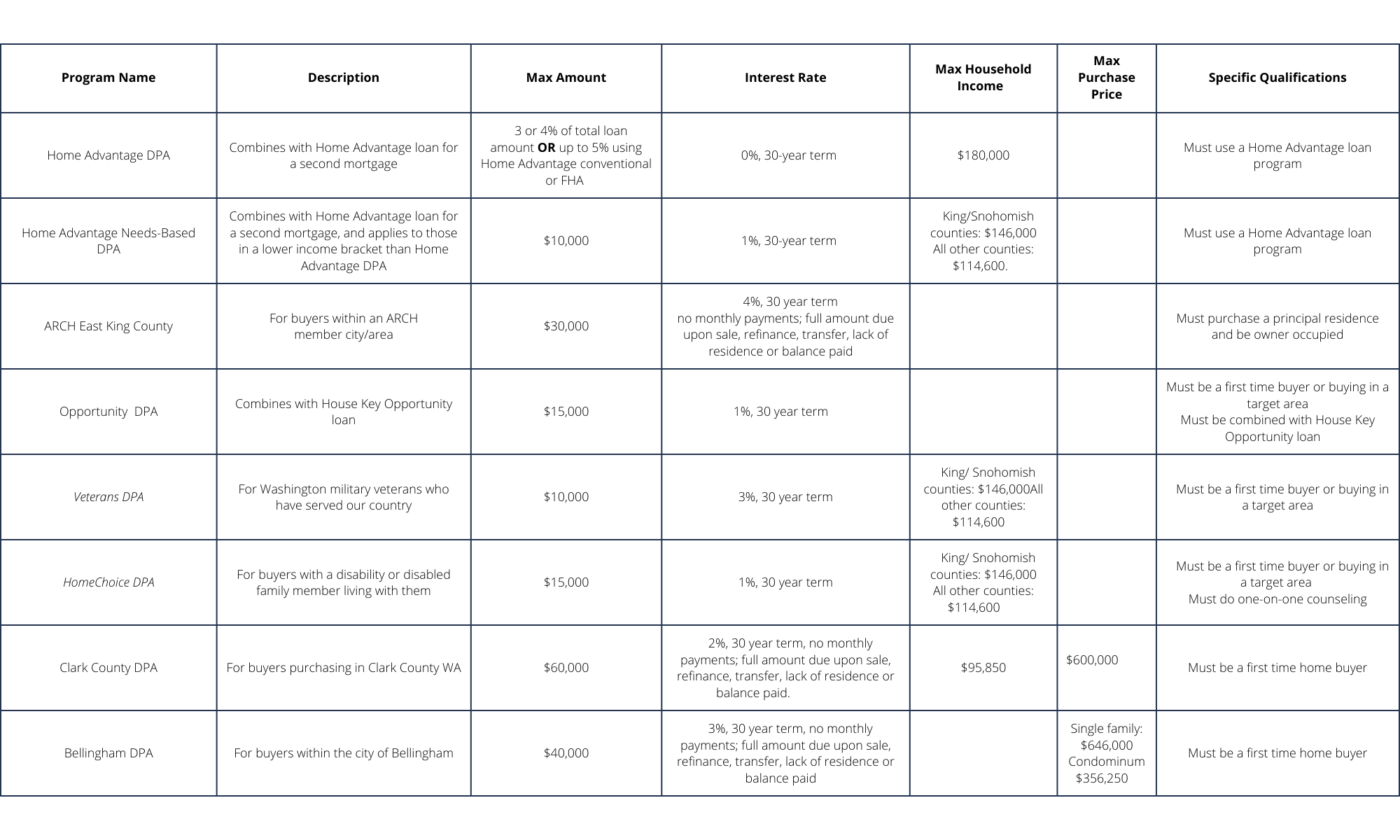

In addition to loans, Washington state offers several different Down Payment Assistance options. With any of these programs, applicants must attend an educational seminar, meet income maximums and work with an approved loan officer. Some DPA programs are specifically for veterans, disabled persons, or even for specific areas like the city of Bellingham. Every DPA loan will be wrapped into one of the two home loan options, meaning you’ll just pay one monthly amount for both loans combined. Each DPA option and its requirements are outlined below.

Individual banks or credit unions may offer their own programs to first-time buyers as well, if you’re curious about what your personal bank might have, meet with a lender to discuss options.